A 36 Month Investment Lesson

By Handzalah / Black Swan Research 26 March 2026, 3:45am MYT

how it started

During the end of 2025, creeping up till today, the time I am writing this, I had realized a large flaw in my investment philosophy. Despite listening to and reading a bunch of materials on famous investors such as Warren Buffet, Charlie Munger, Peter Lynch, Monish Pabrai, Guy Spier, Terry Smith and recently François Rochon, I had far great of a confidence, thinking that picking the right business was easy. Coming from few courses taken in university relating to corporate finance and valuation had made it seem way too easy. Just plug some numbers and assume certain assumptions, BOOM, you get the estimated valuation of an entire enterprise.

Obviously, this was a very wrong and flawed way that we are being taught. It is not the fault of our lecturers but rather the material that is being transmitted. It makes finance seems like a black and white kind of exercise. My best example of detrimental flaw within the corporate valuation class is the going concern assumption. In our valuation models we plug in that terminal growth rate should equate to that of the country’s GDP growth rate. The fundamental flaw within this assumption is the assumption that businesses, regardless of their economic qualities, grow indefinitely. This is a very wrong assumption especially in our high-paced capitalist market today. Many business good and bad have went bust. Disruptions can lead to many business to abandon their position in the market. In a capitalist economy, most business do not survive more than couple decades, let alone 100 years. Despite this, we are taught that all businesses deserve a terminal growth rate above 0%. This is not to say that all businesses are going bust but rather only a few great business with great economic moats and qualities are deserving of the assumption of positive terminal growth rate.

Another related flaw is my attachment to numbers. I would spend most of the time researching on their financial numbers and gathering data to forecast. This would eat up a lot of the time as I would often adjust the numbers every time a dataset would change. For instance, if the US fed fund rate (FFR) changes, my whole valuation would NEED to change because the FFR would shift the risk free rate calculation part in the weighted average cost of capital (WACC) section of my valuation model. So my focus was on the numbers. I really wanted to polish the valuation models. The problem here is, your valuation “forecast” will probably not materialize the way you entailed it in your valuation forecast. Management of the businesses themselves do not know the right growth rates or margins let alone a retail investor who does not have additional information but that which has been made public. Therefore, it is my belief that investors should not focus on forecasting the numbers but rather study the dynamics of the business model and the sustainability of their numbers. A great business with a “great economic moat” will most likely continue to compound their earnings indefinitely, sustaining their great numbers at the same time. This is where investors must focus, whether the great financial performance can be sustained for decades.

Shift in focus

After realizing the grave investing sin that has been committed for approximately 3 years, I have changed and restructured my investment philosophy and investment portfolio. From the focus of getting the numbers right to studying and researching about what can disrupt the businesses’ compounding their earnings. The shift meant that some of my investments would have to be sold because it is not within the investment framework anymore. Now businesses that are, based on my judgement, able to hold their market position for decades, are held at a higher status in terms of investment attractiveness.

Lowering the numbers of time spent on assumptions and forecasting saved plenty of hours which was then channeled back to truly understanding their economic and business landscape. Investors should worry more about if they business can fend off competitors and how they differ to one another. If it seems too difficult, then it is better for you to avoid it.

In 2023, I had invested in a company where the main investment thesis was around their growth in dividends. I had assumed that their dividends would just keep growing proven by their track record. At the same time spending my only 20% of the time researching on how their business model works. They manufacture goods. However I do not know their position in the market. Are they a low-cost producer or do they benefit from supplier network. I do not know what keeps them away from competitors. Up till the first quarter of 2026, I still had not found what keeps competitors away from eating their lunch. Therefore the divestment of the company led to a huge relief.

Fortunately, near the end of 2025, I had found a great investment where the economic qualities of the business was clear. The business gave me reasons to believe that it can last for decades. Their business involves the government granting the concessions for operating within the airports around the Saudi Arabia. Now these grants are not easy to come by and the government do not just give grants to anyone. This alone already creates a large barrier to entry. This is evident by their great market share within the business they do of around 95%. Additionally, the company is partially owned by the Saudi government making it extremely hard to compete against. Couple the barrier to entry, government support, and the structural growth (i.e. e-commerce growth in KSA), it is fair to assume that they have the economic qualities to ward off the negative effects of capitalism.

Investors should see the great differences between the investment thesis of my investment in 2023 compared to my investment thesis in 2025. Know where to focus. Always challenge your thesis. And be patient because it is time that is the one of the largest factor in your returns as an investor.

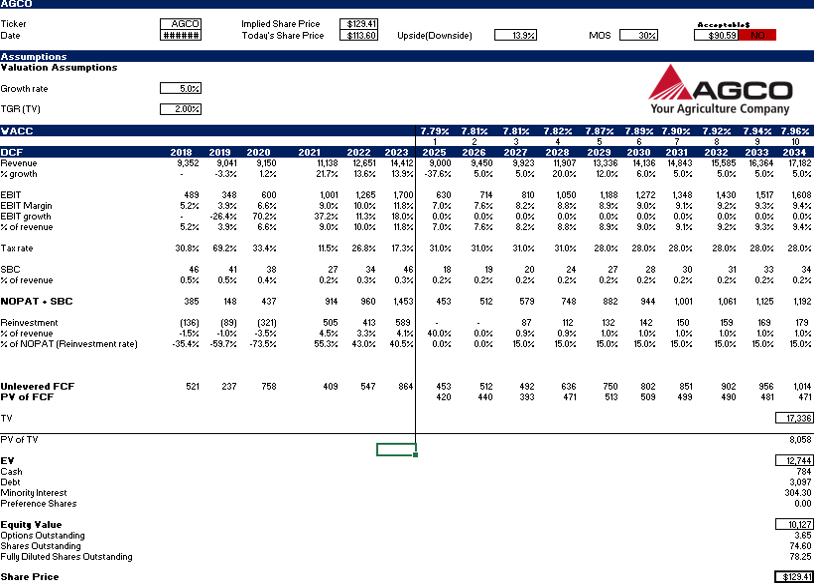

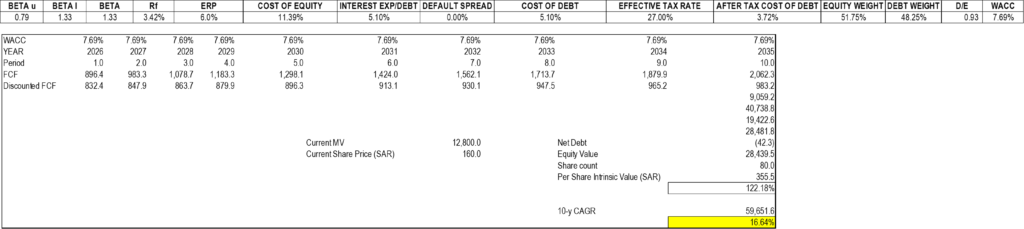

2023 Valuation model

As you can see from the two images above, I tried to model the WACC for each year and try to get all the small details. Now you should beware of sending too much time on the numbers as I have repeated many times. It is alright to get a rough estimate.

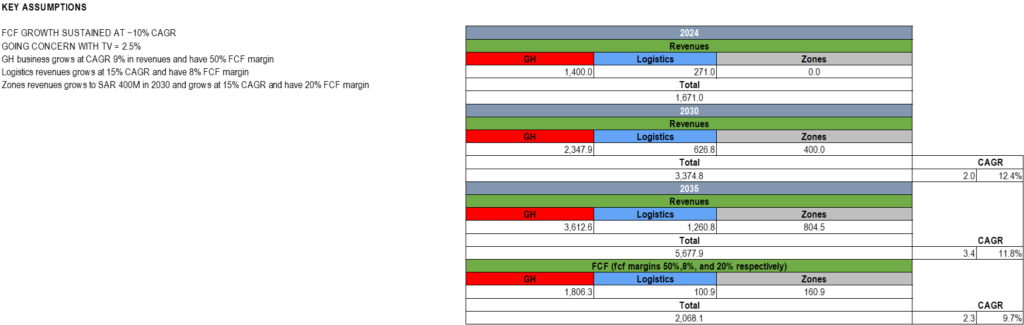

2026 Valuation model

During 2026, valuation is now considered but is not assumed to be a certainty. Therefore rough estimates will just do. Energy and time should be spent on their economic qualities. Despite 2026 valuation model seemingly being still complicated, it is also important that you perceive the data with caution, knowing very well that the future of the business may not go as you planned it to. I do not take the numbers as a truth but rather as a rough estimate on their company value.