Focus Point Investment Thesis: Management’s Farsighted Nature Trump Myopic Mindset

By Handzalah / Black Swan Research 2 April 2026, 1:25am MYT

business overview

Before I start with my investment thesis and overview on the company, I want to clarify this is not an investment advice. Recognized as the largest eyewear retailer in Malaysia with more than 200 outlet nationwide, Focus Point leads the fragmented market with approximately 7% market share. This seems to be a smidgen in the grand scheme of things. However, the eyewear retail market is very fragmented therefore to attain a higher market share than what Focus Point already hold is an extraordinary task. The low barrier to enter the business is one of the causes for the high fragmentation. Started in Muar, Johor back in 1989, Dato’ Liaw Choon Liang, the founder of the business is still the CEO. Liaw owns approximately 51% of shares in the business (direct and deemed interest). Their main business segment is the retail of eyewear which includes contact lens, sunglasses and prescription glasses. They have a F&B arm that makes up 15% of revenue in FY2024. The F&B business is mainly a bakery by the name of Komugi. In one of Warren Buffet’s letter to shareholders, he said “buying a retailer without good management is like buying the Eiffel Tower without an elevator.” This emphasizes the importance of management when it comes to retail, as it is a business model filled with rivalry and competition. And based on my experience with the founder and CEO, Liaw seems to be a very competent manager of the eyewear retailer, not to rash with decisions and do not try to predict or forecast greatly which signals that he is a long-term focused leader of the business. I was able to gather such judgment from a post-AGM interview that was streamed on You Tube.

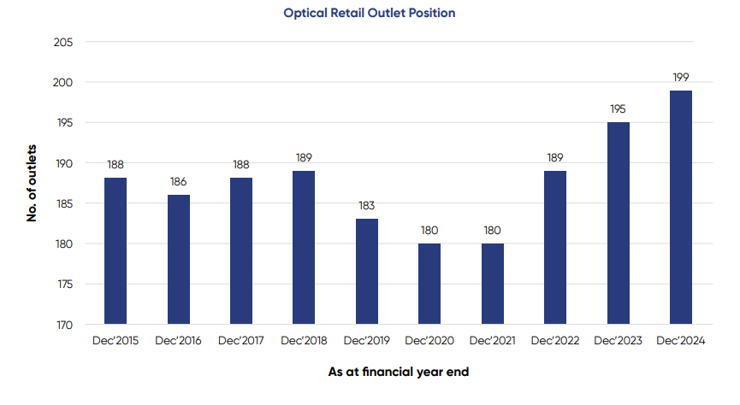

The above figure shows the expansion in retail outlet of their optical segment. The few times of declining store count was their restructuring and disposal of inefficient stores. I would like to keep this as concise as possible therefore I will leave out the depth of the business (i.e. going into detail above their brands and the F&B segment).

Investment thesis

Focus Point is twice the size (i.e. store count) than the second largest optical retailer in Malaysia which bodes well for its economies of scale. Strategically placed at luxuriant locations within the malls across Malaysia, Focus Point benefit from the higher willingness to pay of these demographics. And a greater reach through more outlets mean that they attract more eyeballs, therefore creating a greater likelihood of a potential customer actually purchasing their products.

Furthermore, I believe the eyewear or optical retail is disparate to the overall retail industry. Take the retail for clothes for example, they have recently been seeing a massive exodus of customers from their physical stores. Where did the customers go? They simply have a change in preference and now prefer purchasing clothes online. They are not as hesitant as they was before and not as worried due to many factors. One of it is the great development within the return policy in e-commerce. It is now very easy and convenient to return unwanted products back to the seller. And I believe e-commerce creates a kind of flywheel effect. Once you desire for something, targeted ads may increase you impulse to purchase a certain product. And once that product arrives in a swiftly manner, their satisfaction grows and the yearning to experience it again continues. E-commerce has disrupted most of retail businesses. If retail managers failed to adapt, they are akin to that of the dodo bird story. The change in preference to e-commerce was recently further accelerated by the COVID-19. Now why would do I think optical retailers differ to that of any other retailer? I believe that the process of purchasing prescription lens and even sunglasses is better done physically. And confidence in purchasing the prescription online is weak, at least for right now. An American company tried to restructure their whole business to mainly sell online, however this was not received well by the masses and they continued their expansion in physical outlets. I would like to caution that this may not last. There could be a time where people are fully confident in purchasing prescription lens online. That is amongst the great risks of such investment.

Management holding a large portion of shares outstanding brings confidence to shareholders. ~51% of shares held by Liaw, the CEO and founder, means that he has skin in the game. And based on his temperament and long-term mindedness, I condone the management and their vision for the future of the company.

Additionally, structural tailwinds such has the genetic prevalence of myopia in Malaysia, population growth, and the increase in activities that are theorized to increase likelihood of myopia (i.e. looking at near objects), provide the whole industry sustainable growth.

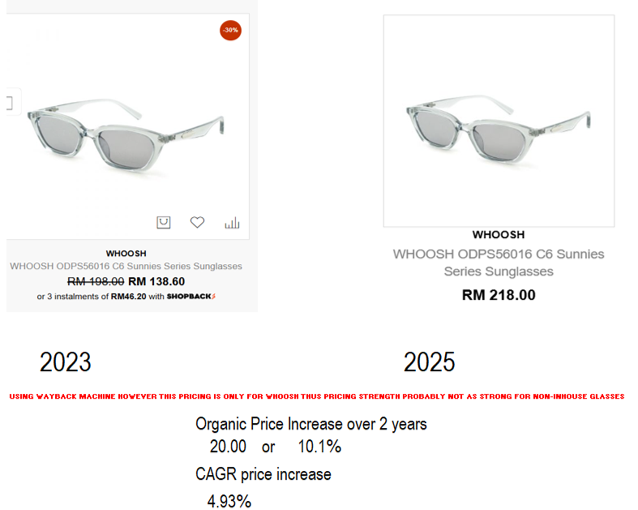

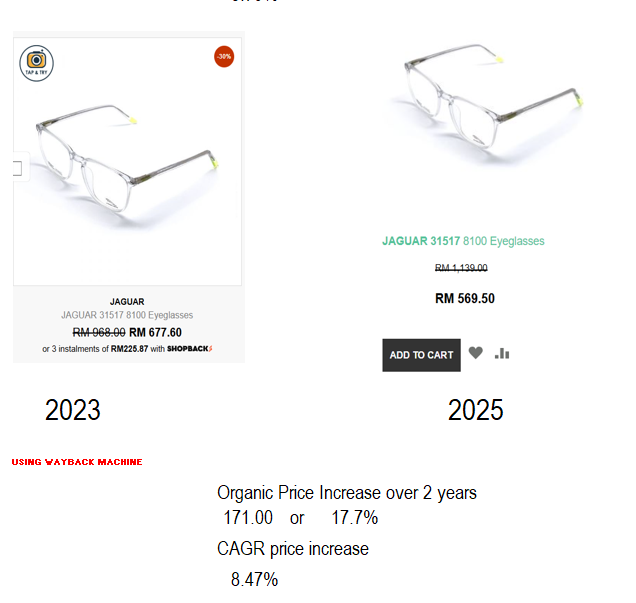

Warren Buffet invested in See’s Candies due to the strong pricing power they have. Similarly, Focus Point has exhibit similar growth due to pricing power. I estimate their pricing power via the use of the wayback machine , calculating that on average they can raise 3% per year in prices. Below are some examples of why I came up with 3%. Price change was calculated based on their original price for the year and not the discounted or sale price.

Lastly, their valuation is one of the biggest element to what makes Focus Point very attractive as an investment. As of today’s prices, they are trading around 25% FCF yield. In other words, if you assume that Focus Point’s FCF will have zero growth and you assume them to still be trading at a 25% FCF yield, you will receive your principle by the 4th year. That means beyond the 4th year, the earnings they make is your profit.

With a very high payoff and a small downside, Focus Point exudes Nassim Taleb, the author of The Black Swan. Nassim Taleb gave us remedies on how to avoid predicting things that are too complicated like economics and markets. One of the remedy is to expose yourself to events that have a potential for high payoff and the downside is limited. I see that Focus Point as an investment is a great example for Nassim Taleb’s remedy.

valuation: estimating growth rate

3 factors for Fous Point’s growth rate and their assumptions

1) Increase in myopic prevalence within Malaysia (2.00%)

2) Malaysia’s population growth (1.25%)

3) Price increase of products (3.00%)

—–> Total estimated growth rate (~ 6.25%)

Population growth rate and the rate of increase in myopia prevalence was estimated. The latter was estimated roughly estimated using an article that measured average prevalence of myopia in certain regions over a few decades. The estimate of 2% was a result of anchoring the numbers given in the article. Added to it a few basis-points in order to be in-line with our theory that the prevalence in Malaysia is above average. The overall estimated growth rate sits at ~6.25%.

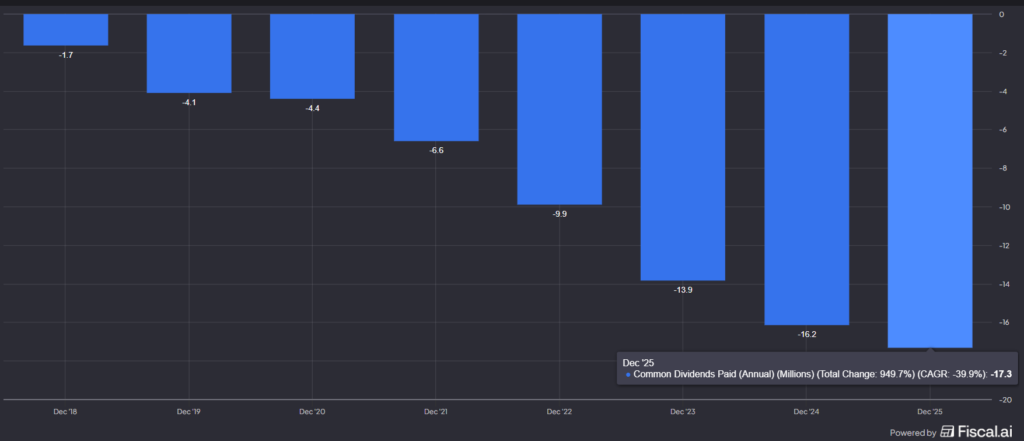

Dividends grew to RM17.3 million in 2025. An increase from RM1.7 million in 2018. This computes to a ~39% CAGR in dividends for the past 7 years.

valuation: model

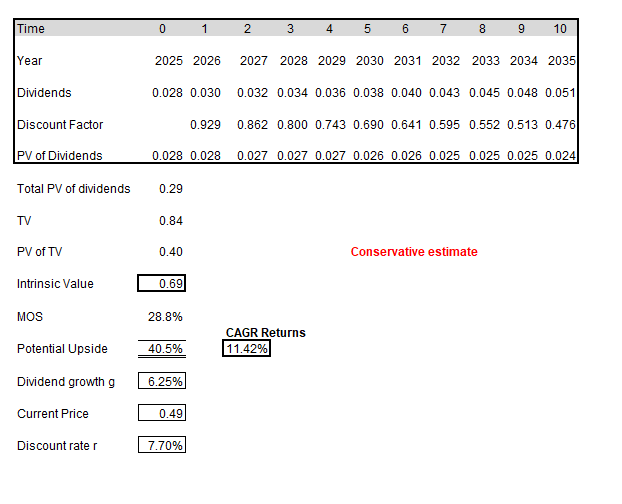

valuation: conservative model

In this model I use the dividend discount model (DDM) to get the intrinsic value. Remaining conservative, I used the growth rate = 6.25%, computed above as the growth rate of dividends. This is way lower than their 39% CAGR in dividend growth for the past 7 years. But I believe this model map out the structural growth via the 3 growth factors mentioned earlier. With this model we get a 10-year CAGR of 11.42%, which is really alluring because we are assuming that the dividends will grow only by the structural growth rate.

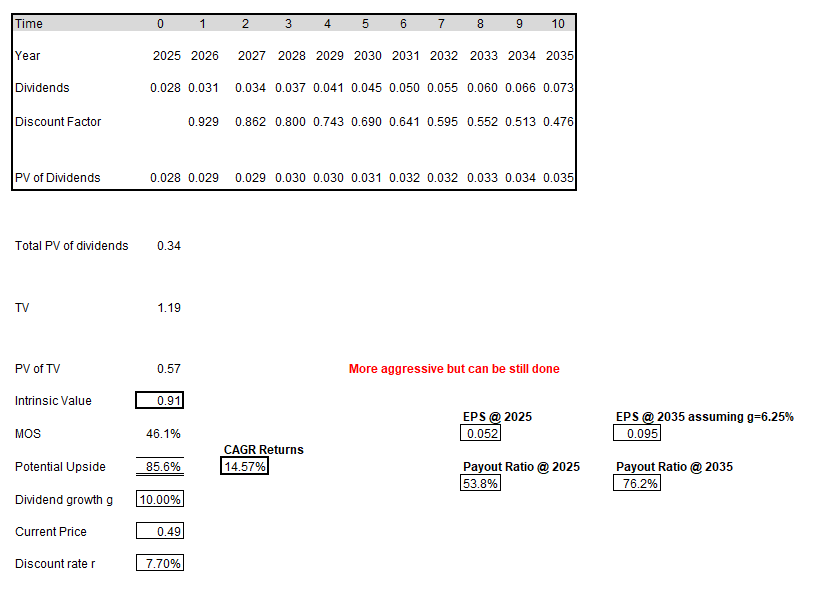

valuation: more aggressive model

This model is only slightly different from the first. I used DDM, however, for this model I assume that their pace of increasing dividends exceed their pace of growth in earnings per share. Assuming earnings per share grow at our structural rate of 6.25% and assuming the growth in dividends is 10% CAGR, the payout ratio will differ. In 2025 the payout ratio is initially at 53.8%. This then increases to 76.2% as the growth in dividend distribution increases over the rate of 6.25% (EPS growth rate). If the structural growth of 6.25% is achieved, I believe they can grow their dividends at 10% CAGR for the next 10 years. 76.2% as a payout ratio is higher than the 53.8% that it started with, however it is not impossible to achieve. And perhaps when they reach close to 70% to 80% payout ratio they may slow their dividend growth rate. But for the 10 years proceeding 2025, it is not unachievable. Keep in mind that the structural growth rate is a very conservative figure. With such assumptions, the expected growth in your investment can be close to 15% CAGR for a 10-year period. This is extremely attractive as a CAGR of 15% will double your investment every ~5 years.

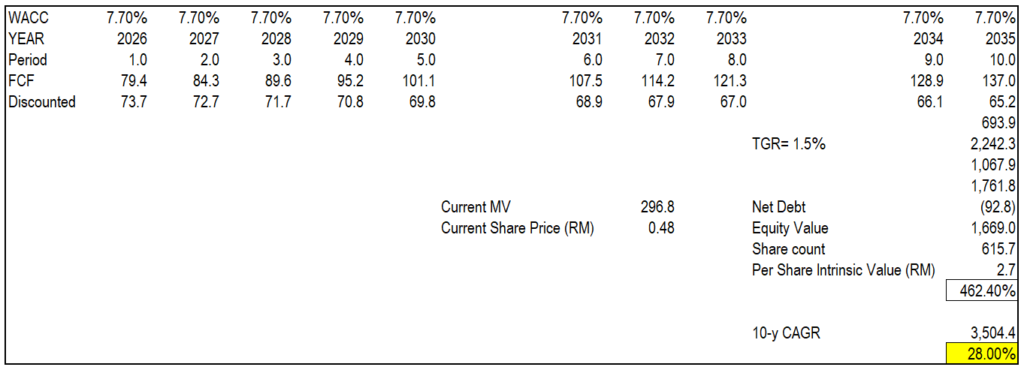

valuation: high payoff

For the last model, I used the simplified discounted cash flow model (DCF). The main assumptions are i) FCF grows at the structural growth rate of 6.25% ii) WACC like the other models were computed to be 7.7% (I will spare you the details to this calculation) iii) the terminal growth rate is 1.5%. Once again, these assumption are not exorbitant or exuberant, they are modest and achievable numbers, at least to my personal judgement. With the assumptions, I got a 10-year CAGR of 28%. This means a RM 1,000 investment will compound to reach a value of RM 11,806 by the 10th year. I need to clarify again. This is not investment advice and these numbers should really just be a rough guide for their valuation. The qualitative features hold more weight. Keep in mind for the DCF or the 3rd model we used RM 0.48 as the current market value per share. The models were measured in different time period but the slight decrease in current MV do not have a large impact on the final intrinsic value.

valuation: low downside

I use fiscal.ai, once again for a clear visualization on certain metrics. The blue is the total assets, orange is the liabilities, and the purple is the equity (in order from left to right). The green line represents the company’s price-to-book ratio which is exceptionally low at 1.94x. This provides some sort of downside cushion or minimizes our downside. Again I would like to direct your attention on the fact that the valuation (with conservative assumptions) generates us an intrinsic value much higher than current market capitalization whilst having a low downside risk. This is as Nassim Taleb advocates, have exposure to large payoff (large payoff means that the payoff potential is not bounded) and low downside (Focus Point trading at sub 2x PB ratio signals low downside).

Overall, there is many reasons for me to believe that Focus Point can compound their earnings over the long-term. Given the strong management and emphasis on long-term benefit, I can say that they have position themselves to fare way better than those who have a myopic view of their business landscape. Risks and uncertainties will always be a part of investments, however having a large payoff and minimum downside exposes us to the beneficial risk management where overconfidence in the knowledge of things do not crowd judgment.