Iran War Effect on Air Cargo Market

By Handzalah / Black Swan Research 7 April 2026, 11:34pm MYT

13% of the world’s air cargo capacity is held by the Middle Eastern carriers. This includes Qatar Airways, Emirates Skycargo and Etihad. Henceforth, the disruption caused by the Iran war on the 28th of February, led to substantial changes in the economics of air cargo and in general logistics. Just prior to the war, IATA released results for February 2026. Air cargo grew a whopping 11.2% compared to the same month last year. Iran’s retaliation had direct consequences on air cargo. Several airports in the Middle East was closed. The airport in Dubai suffered from a drone strike. The implication of global traffic also was significant because the Middle East region houses, the airport hubs located in Dubai, Doha and Abu Dhabi. The fleets were also being grounded which affected 13% of global air cargo capacity.

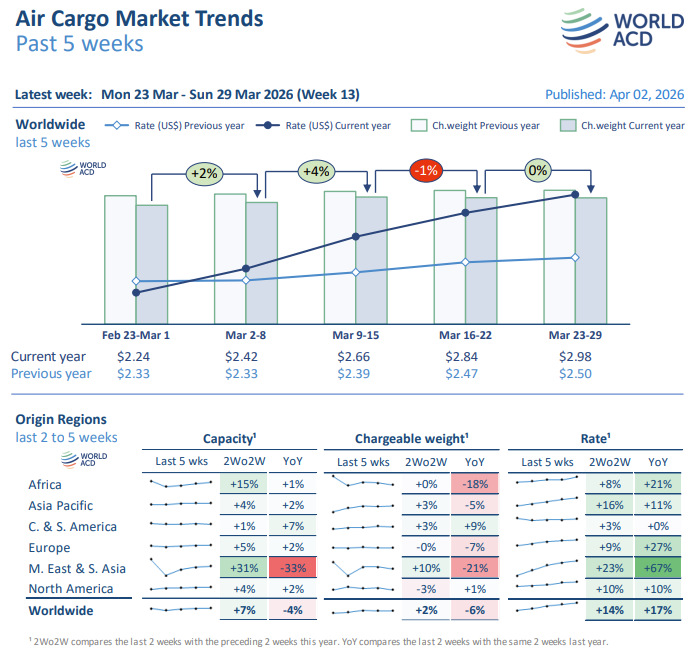

World ACD releases their weekly air cargo trends every week. The next section will broadly summarize their reports.

Week 9 (Feb23-Mar1)

Initial impact of the war was not clear because based on the data of Feb 23 to Mar 1, it only captures 2 days after the initial attacks. In the Middle East & South Asia (MESA) region on February 28th, they experienced overall airfreight related exports plummet -27%. The following day falling by -56%. This totals the combined drop of -40%. Chargeable weight also declined for cargo out of South Asia to Europe and US.

Week 10 (Mar2-8)

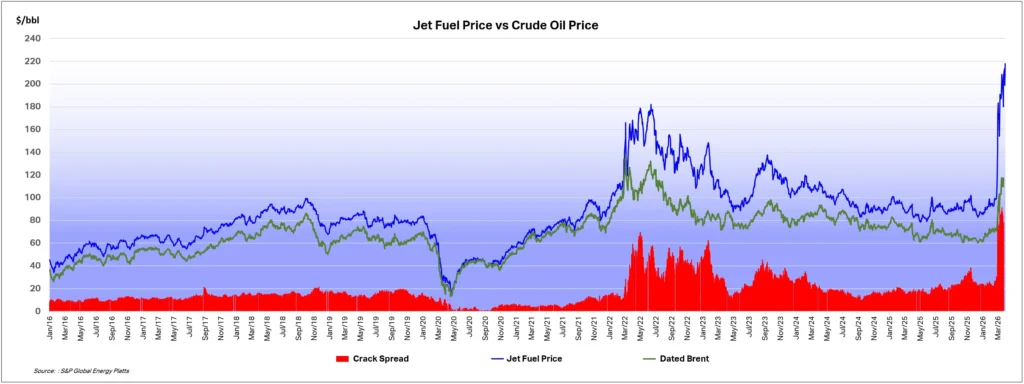

Rates keep increasing to $2.40. However there is a temporary lowering of capacity due to the air space and airport shutdowns in the Middle East. Overall global airfreight traffic dropped -4% WoW or -12% year-over-year (YoY). Lower flight due to shutdowns can be seen by the decline of -36% WoW in chargeable weight for MESA region. Africa was also significantly affected with a decline of -23% WoW in chargeable weight. Capacity declined a whopping -42% WoW for MESA. This shows that in the MESA region, there is an increase in airfreight load factor or the utilization of available capacity. Gulf region had severe decline in outbound volume falling by -62% WoW and capacity falling by -70%. Again the slightly better volume or chargeable weight figure relative to the capacity shows that their load factor was better. After the drone strike in Dubai’s airport, carriers and forwarders mitigated their risk by using regions like Saudi Arabia as an alternative gateway. Additionally, they added charter capacity and increased their trucking activities. The loss in capacity drove airfreight rates higher. Average global rate was increased by 6% WoW. MESA rates rose by 28% WoW or 20% YoY. Few airlines announced that there will be an increase in their fare in their passenger operations due to the monumental increase in jet fuel price (up 58% WoW).

Week 11 (Mar9-15)

Rates continue to rise to $2.67 despite the recovery in the Gulf capacity. Global airfreight rate rose 10% WoW after already surging 8% WoW the prior week. The air cargo market is facing headwinds of disrupted markets, constrained air cargo capacity, demand backlogs, uncertainty and higher jet fuel prices. Volumes in MESA improved by 30% WoW. This shows the recovery in Gulf capacity. In MESA region airfreight rates increased another 22% WoW to $4.37 per kilo or up 58% YoY. Air cargo capacity and traffic improved with the aid of partial opening in some airports and airspace, as well as alternative routes which avoid restricted areas. Jet fuel prices continues to climb up as prices increased by an additional 11% WoW. That is an increase of 94% or close to double their pre-war level. Some carriers and airlines may start implementing air cargo fuel surcharges along with war-risk surcharges which will contribute to increasing overall air cargo rates.

Week 12 (Mar16-22)

Global rates continue to climb to $2.84. This is a week-over-week increase of another 7%. The average worldwide spot rates is 26% higher than same week last year. However, MESA region faced a sharper YoY climb in rates of 70%. And a WoW increase in rates of 22%. Capacity in MESA dropped in week 8 to week 10. However there is stabilization in week 11 and week 12 with capacity increases amounting to 6% WoW and 2% WoW respectively. However the capacity of week 11 and 12 combined is still down -37% YoY. There is some operational restrictions when operating to and from Gulf markets, therefore it means that most European and North American carriers are not operating in that region.

Week 13 (Mar23-29)

Further increase in global airfreight rates to $2.98 slowed the air cargo market as price for transporting goods remain high. However, the rates increase despite the rebound of airfreight traffic which suggests that the increase in rates is primarily coming from price of jet fuel and lesser from the capacity constraint. The global rate increased but at a slower rate. An increase of 5% WoW for week 13. The is in contrast to week 12 which saw an increase of 10% WoW in global airfreight rates. The price of jet fuel more than doubled reaching all-time high in March. The MESA region has seen capacity increased 31% 2 weeks-over-2 weeks (2Wo2W) or a decrease of -33% YoY. This shows an improvement over the last 2 weeks but still not at pre-war levels in terms of available capacity. MESA chargeable weights increased 2Wo2W by 10% but fell -21% YoY. Again signifying a recovery over the fortnight but not near pre-war levels. The lower decline of chargeable weight to the decline of capacity indicates that the load factor improved or that more planes that are operational have higher utilization rate of their available capacity. Rates for MESA increased 23% 2Wo2W and also increased YoY by 67%. This signifies the effect of capacity constraint and higher jet fuel prices on the air cargo market.

With these set of data in mind, it still remains uncertain as many factors are at play. The increase in rates may mean that the price trickles down to the consumer. This can influence the inflation rate. Jet fuel prices also increases the prices of essential products such as fertilizers. If this continues, farmers will likely see lower production which can lead to an increase in food prices which can directly affect the rise in inflation rate. The dependencies of countries to each other created through globalization and how war can disrupt the benefits of globalization through higher energy costs is a proof to what Nassim Taleb said in the book “The Black Swan”, whereby lower volatility does not mean stability or assurance because once a black swan event occurs, the catastrophe causes fundamental shift in how the economy works. Therefore, risk should not be measured by the nature of volatility.