Berkshire Hathaway Lessons: Margins Are Not the End All Be All of Business Quality Assessment

By Handzalah / Black Swan Research 17 June 2026, 7:05pm MYT

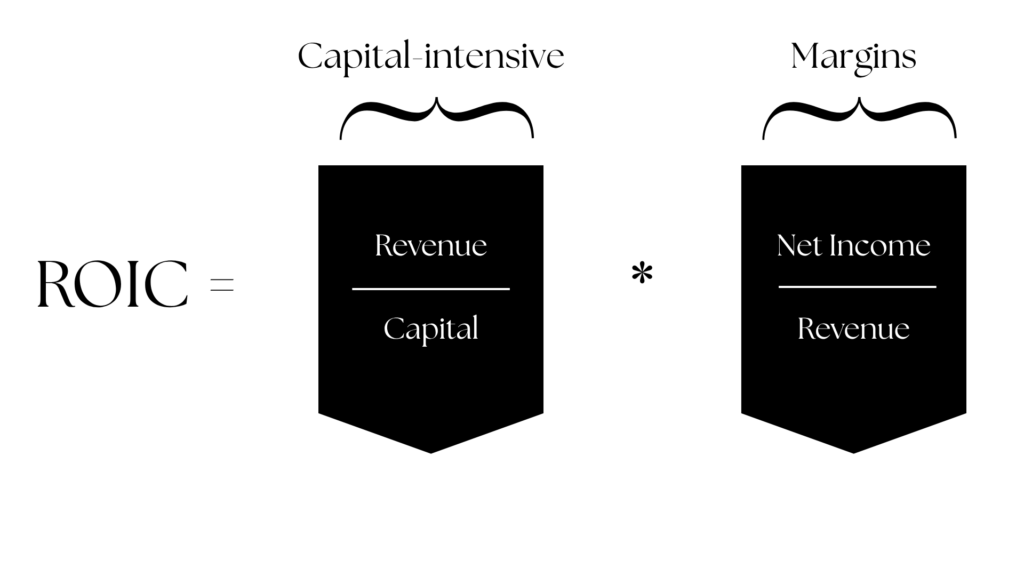

A business is not necessarily bad or of low quality if it operates under thin margins. The absolute level of profit margin is relatively unimportant. What truly matters is the return on invested capital (ROIC). For every dollar invested, how much dollar of return can it produce? Investments should assessed by their capital. The investment is attractive if the ROIC is above your hurdle rate. What we can learn from the early years of Berkshire Hathaway is that investing in capital intensive business or thin margin business does not dictate the quality of the business. One must look at the overall picture. If the business can squeeze a small profit margin but require minimal incremental capital, this may be an attractive investment as the overall ROIC is satisfactory. Alternatively, a business can require heavy capital investments but have high margins which makes up for the high level of capital requirement.

The textile business was a poor investment as required high capital investments which yield low profit margins. This is in contrast with Berkshire Hathaway’s more recent businesses like their regulated capital intensive businesses, which consists of railway company and a utility company. This regulated capital intensive businesses require heavy capital investment but the overall ROIC is more than satisfactory as their margins pushed the ratio higher. The qualitative aspects of the business like how its regulated with high barriers to entry makes it more attractive. Their ability to reinvest large sums of capital is also another reason why Berkshire had purchased such businesses.

On the other hand, See’s Candies was a business which required very little capital and had high margins which translates to a very high ROIC. Such businesses are exemplary and very rare. However, businesses like See’s struggles to grow as their reinvestment opportunity is minimal. However, because See’s operates under a conglomerate, Berkshire Hathaway, the benefit of being able to redirect capital from See’s to other businesses that have greater returns on incremental capital adds a competitive advantage for Berkshire.

To reiterate, it is not that important for a business to yield high profit margins on its own but rather have high returns on invested capital. This is the metric the Buffet has focused on over the years. Furthermore, it is important to take the businesses’ qualitative advantages and disadvantages into consideration. Do they have the ability to fend of competition? Are they able to increase their product prices over inflation? Is foreign producers eating up their market share? Questions like these should be pondered upon as they truly guide an investor on his journey to finding great businesses.