Valuation Blunder: Using Metrics That Do Not Reflect Economic Reality of a Business (Focus Point)

By Handzalah / Black Swan Research 21 June 2026, 5:15am MYT

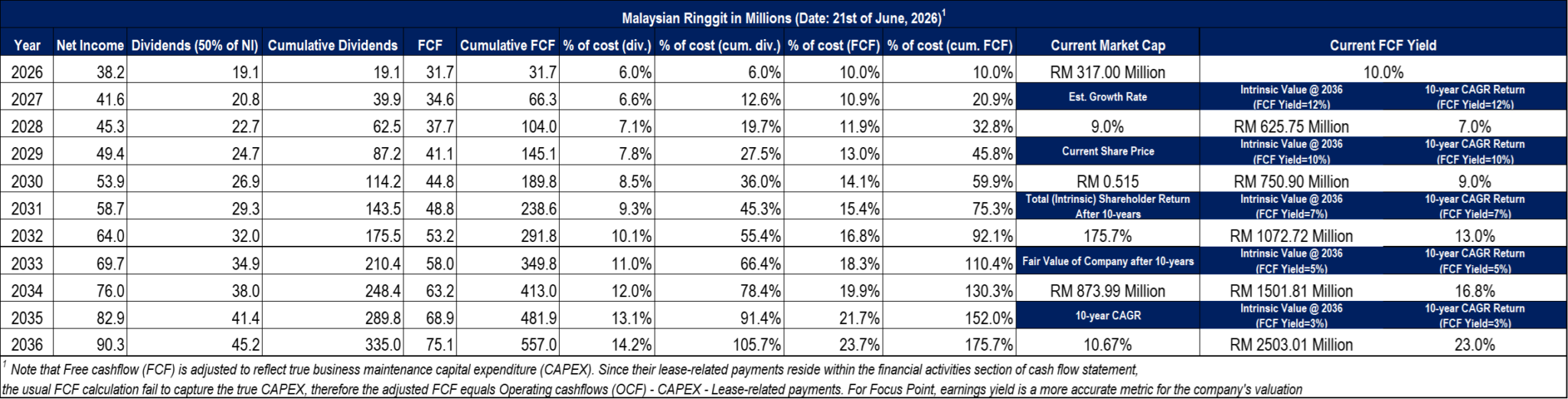

It is not my intention to startle you with the table above filled with various jargons and numbers. However, it is important that I share my blunder within the calculation of Focus Point’s valuation using free cashflow (FCF). You see, the footnote of the table above fully describe the failure that FCF brings when calculating Focus Point’s intrinsic value. Since a major maintenance capital expenditure (lease-related payments) actually reside in the financial activities section of the cash flow statement, the conventional FCF understates the true capital expenditure (CAPEX) by excluding lease-related payments. Therefore, just like what is mentioned in the footnotes to the table above, the adjusted FCF is a better metric and more accurately reflect the economic reality of Focus Point. It is calculated by including lease-related payments as part of CAPEX (Operating cashflows (OCF) – CAPEX – lease-related payments). The reason why I say that the lease-related payments are a major maintenance CAPEX is because of the nature of Focus Point’s business model. They lease the shop lots from malls. Without these leases, they simply would not be able to operate their business. Therefore, it only makes sense to include the lease-related payments in CAPEX.

My estimated growth rate for Focus Point has increased from 6.25% to 9.0%. This was established right after their Q1 2026 webcast, where I got further insight in Focus Point’s growth derived from the optical segment. I noticed that their corporate sales portion of their optical segment grew at a rapid rate. Year-over-year (YoY) up around 40%. And the CEO believes that this growth is sustainable, as they continue to attract around 20 corporate customers every month. The main growth assumption for the table is 9.0%. Therefore, FCF and net income is assumed to grow at 9.0%.

Key Takeaways From the Table

- Cumulative dividends (50% of net income because of recent dividend policy changes) received from 2026 to 2036 will amount to RM 335 million which is above the current market capitalization of RM 317 million. This means that, by dividends alone, in 2036, your principle price consideration paid or cost basis in 2026 is covered by your accumulated dividends received. Your dividends accumulated over the 11 years (including 2026) will equate to 105.7% of your cost basis in 2026. Another way of interpreting this is that the value of the company in 2036 is extra to your paid off cost basis in 2026.

- By 2036, your dividend yield on-cost or dividends received in 2036 divided by cost basis in 2026 will be 14.2%.

- By 2036, FCF yield on-cost or FCF in 2036 divided by cost basis in 2026 will reach a whopping 23.7%, almost a fourth of your cost basis in 2026.

- However, cumulative FCF (2026-2036) will reach RM 557 million or 175.7% of your cost basis in 2026.

- The right side of the table shows various intrinsic value estimates. A reasonable FCF yield is likely between 5% and 7%, therefore my estimated intrinsic value will yield around 13% to 17% CAGR.

- Current FCF yield is 10% which is attractive when measured against a ‘risk-free rate’ such as the 10-year bond yield. The 10-year bond yield in Malaysia is currently at 3.61%. The going-in return of 10% is likely to yield at least a satisfactory returns on capital, given that the business continue to thrive (i.e. growing their FCFs).

The Mistake of Taking Conventional FCF Metric as a Measure of Valuation for Focus Point

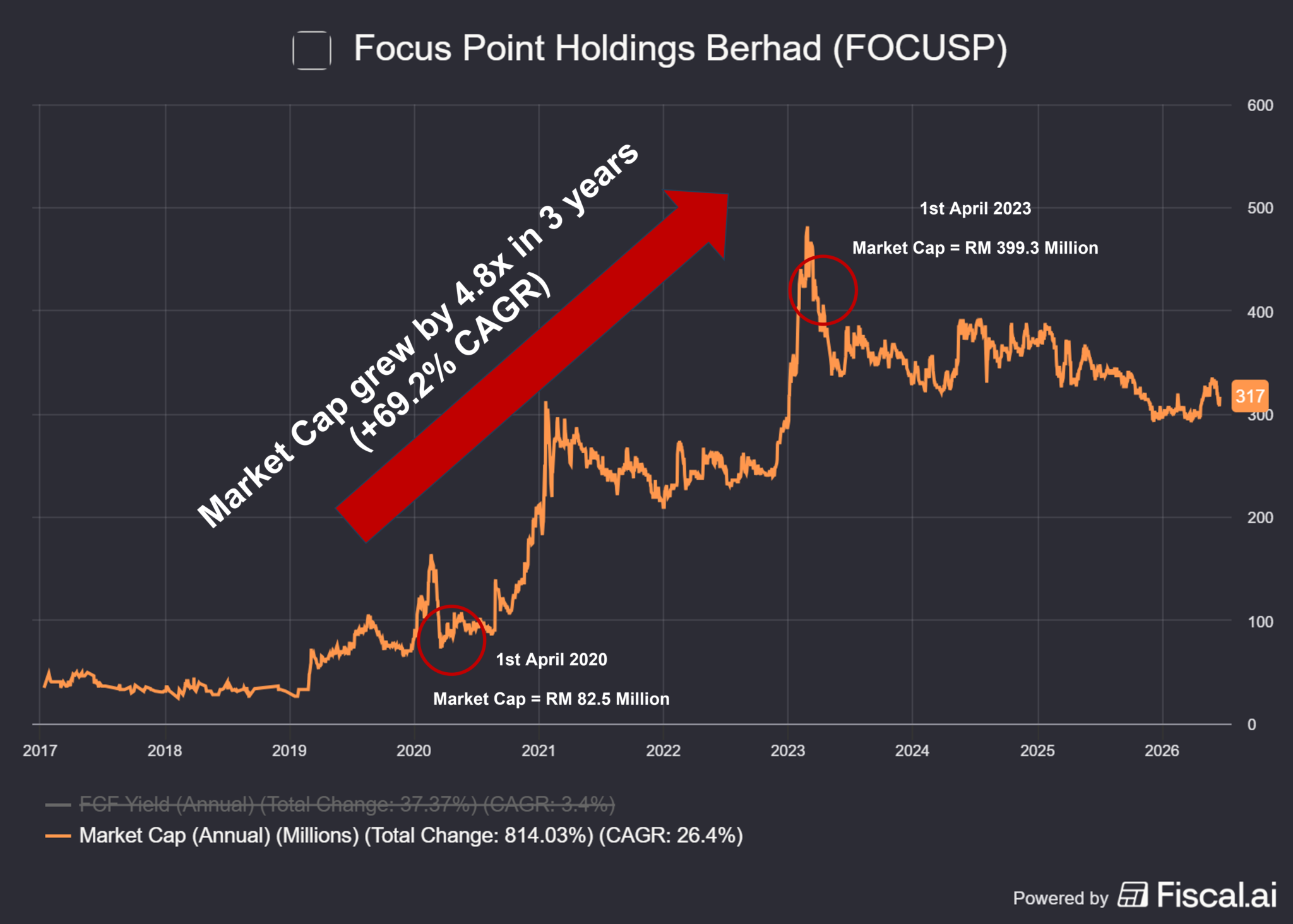

Look at that! The value of the business grew from RM 82.5 million in 2020 to RM 399.3 million in 2023. That computes to a 4.8x in just 3 years. I was curious to what caused such a surge in value for the company. A 4.8x on your capital is satisfactory even if you stretch the time it takes to 4.8x to 10 years.

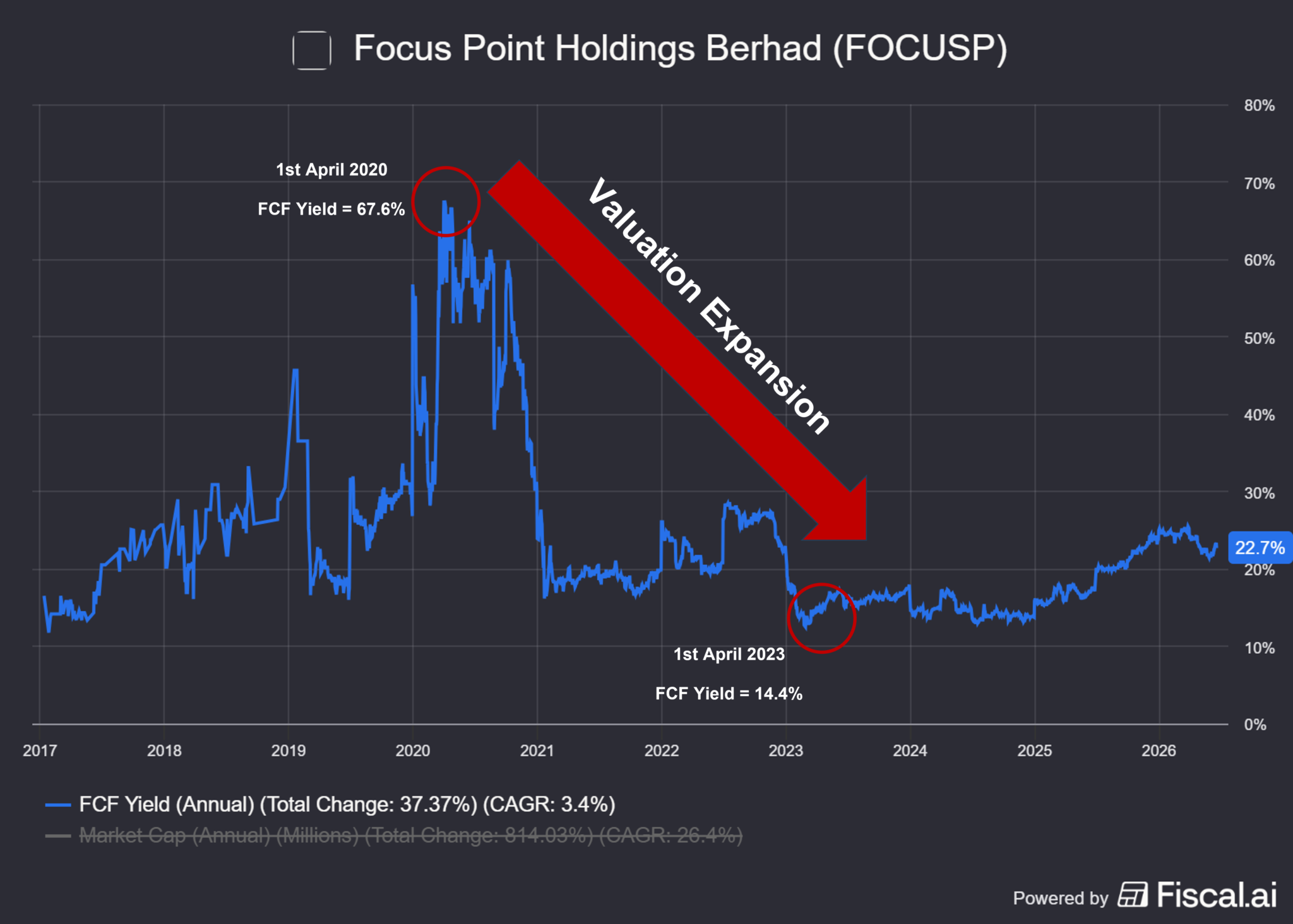

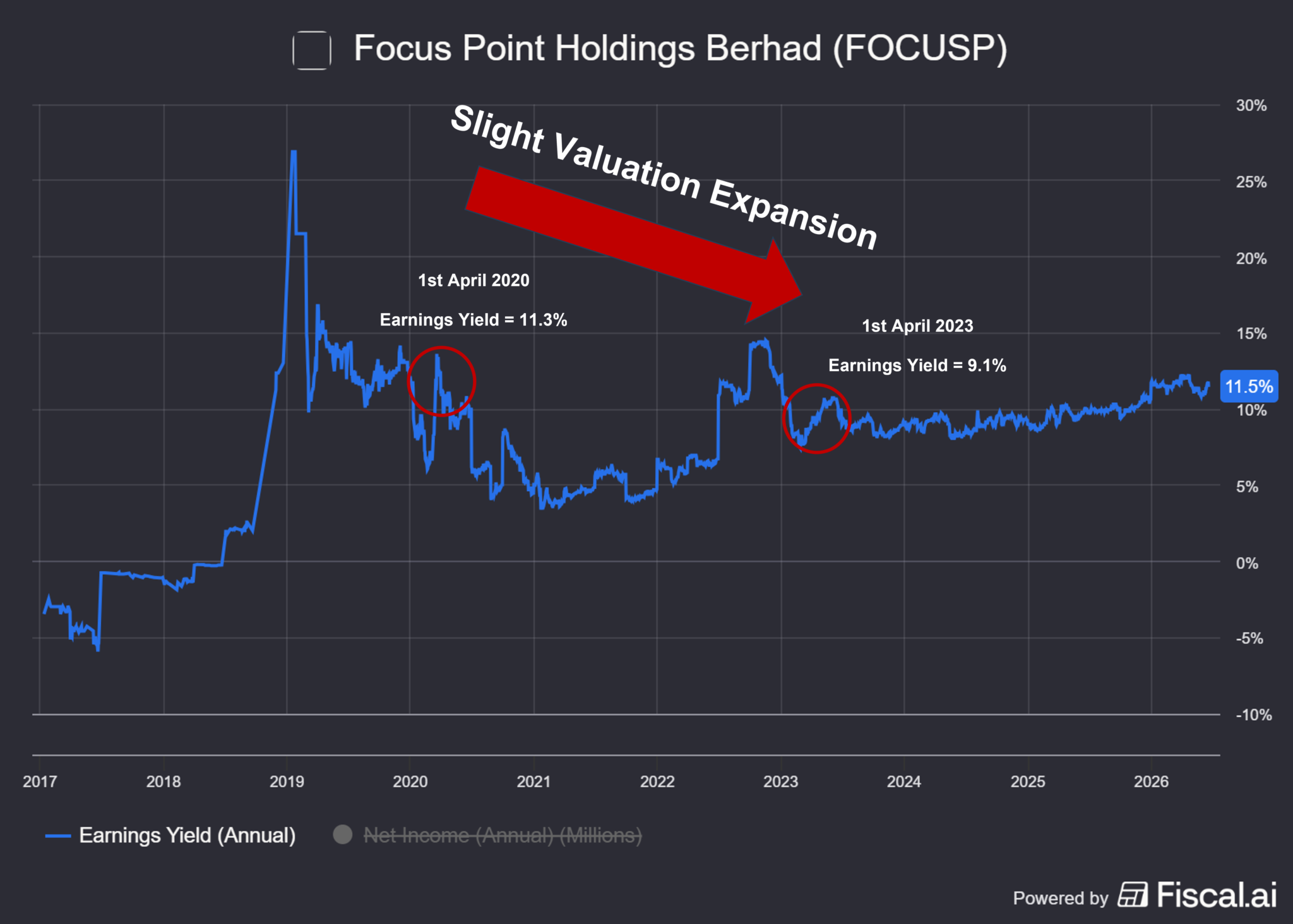

Here is where I made the mistake. Keep in mind that the chart above shows FCF unadjusted, unlike the table that is at the most top of this page. Therefore, the numbers do not really reflect the true valuation. Initially, I thought valuation expansion from 67.6% to 14.4% in just 3 years is ludicrous. I asked, “why did that opportunity exist back in 2020?” How can FCF yield be above 60%? Keep in mind, I thought the growth in the company value was solely from the realization of the market that a FCF of 67.6% is way too cheap. But this is not the secret behind the impressive 69.2% CAGR in market cap from 2020 to 2023. FCF simply do not depict the real business and economic reality as it excludes a major maintenance CAPEX, lease-related payments.

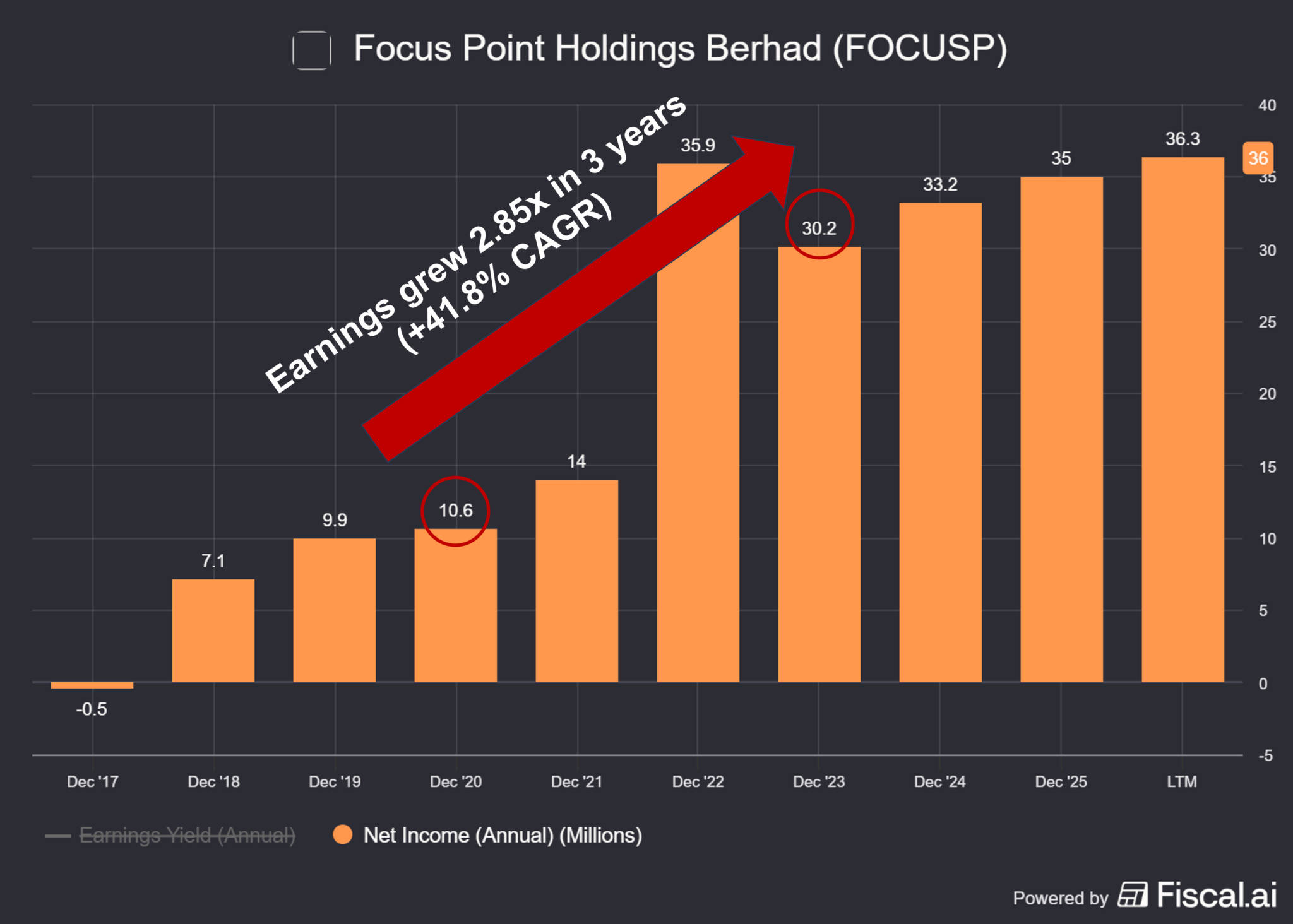

Aha! That is why the value of the company climbed 4.8x in 3 years. It was due to the growth in earnings, which grew 2.85x within the same 3 year time period. This computes to an astounding 41.8% CAGR for the 3 years. Net income or earnings better reflect Focus Point’s actual profitability as it already includes the finance costs (lease-related payments). Earnings primarily influenced the increase in market cap from 2020 to 2023.

With the realization that earnings better reflect Focus Point’s business (compared to unadjusted FCF), I used the earnings yield (inverse of P/E ratio) to find out how much of the growth in market cap was aided by valuation expansion. Unlike the crazy numbers seen with the FCF yield, the earnings yield reflected only modest valuation expansion. Within 3 years the valuation expanded from 11.3% earnings yield or a P/E of 8.85x to earnings yield of 9.1% or a P/E of 10.99x. Again this reflects that the bulk of the change in market cap within the 3 year period is explained by the rapid growth in earnings.

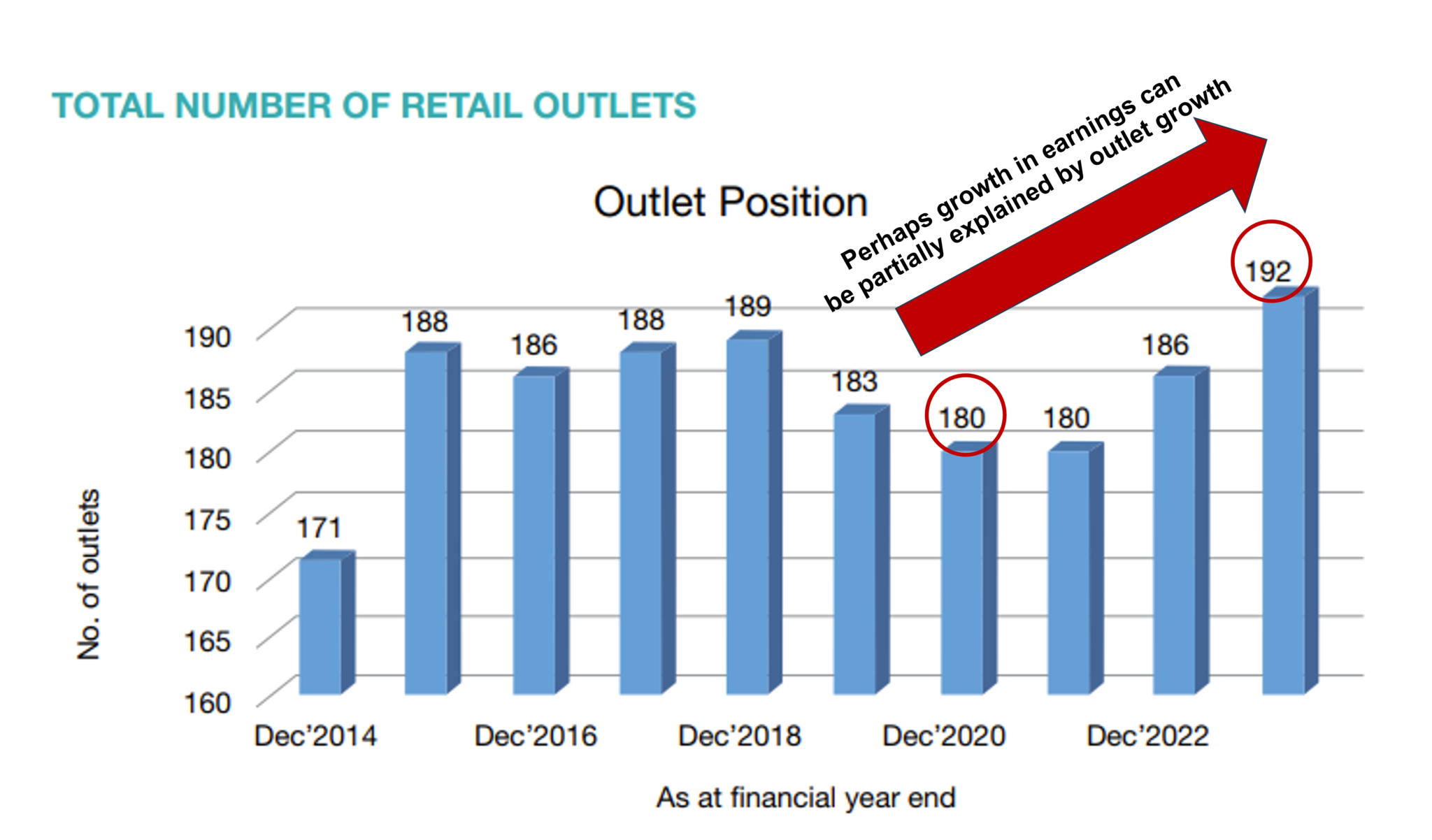

The higher earnings can probably be explained by their growth in outlets over the same 3 year period. They managed to grow their optical outlets from 180 to 192 in 3 years. Furthermore, earnings most likely grew a seemingly rapid pace because of the lower earnings bases in 2020 as people were in lockdown during the widespread pandemic which translate to lower sales volume.

Great Business and Value but Not 25% FCF Yield Great

This was quite an embarrassing experience. How could I have missed that? How did I not realize that leases was a central feature to how their business operated. Moving forward, if something seems too good to be true, I must ask, “why does this investment opportunity exist?” A 10% FCF yield (adjusted FCF) is still attractive and I believe that if the company continue to operate well, shareholders of Focus Point will reap great returns. But it is not as risk-less as a 25% FCF yield business. Therefore, it is inherently has a higher risk attached to it. Back to the drawing board. The hunt to find well-operated businesses at a FCF yield above 20% continues.